What are the 401k contribution limits for 2024 and 2025? This question is on the minds of many Americans, as they plan for their financial future. Understanding these limits is crucial for maximizing retirement savings and achieving financial security. The contribution limits for 401(k) plans can fluctuate year to year, so it’s important to stay informed about the latest regulations.

This article delves into the 401(k) contribution limits for 2024 and 2025, providing a comprehensive overview of the rules and regulations that govern these plans. We’ll explore the maximum contributions for both regular and catch-up contributions, as well as the differences between traditional and Roth 401(k) plans.

We’ll also discuss the impact of these limits on retirement planning and the factors that can influence them.

401(k) Contribution Limits for 2024 and 2025

The annual contribution limit for 401(k) plans is set by the IRS and is subject to change each year. These limits dictate the maximum amount of money you can contribute to your 401(k) plan in a given year, allowing you to maximize your retirement savings and benefit from tax-deferred growth.

Contribution Limits for 2024 and 2025

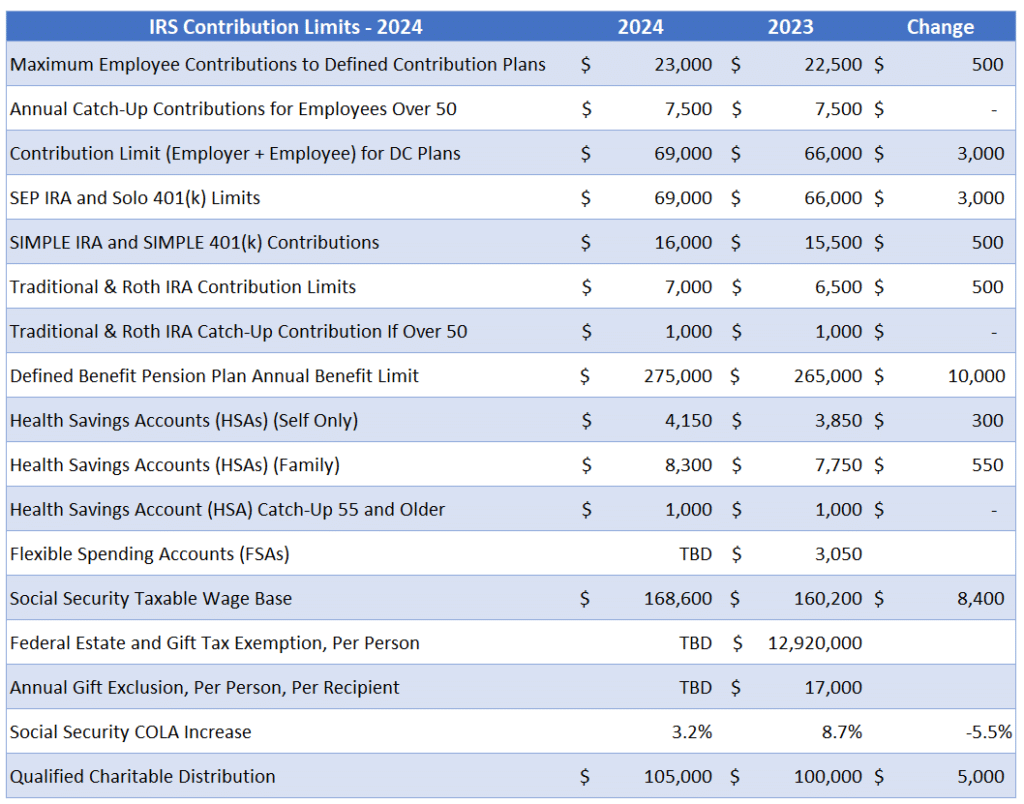

The maximum amount you can contribute to a 401(k) plan in 2024 is $24,500. This is an increase from the 2023 limit of $22,500. For 2025, the contribution limit is expected to increase to $26,000. These limits are for individuals under the age of 50.

Families have different tax situations than individuals. Use a tax calculator for families in October 2024 to estimate your tax liability and plan accordingly.

Catch-Up Contributions

If you are 50 years of age or older, you can make catch-up contributions in addition to the regular contribution limit. For 2024, the catch-up contribution limit is $8,000, bringing the total maximum contribution to $32,500. For 2025, the catch-up contribution limit is expected to increase to $8,500, resulting in a total maximum contribution of $34,500.

The W9 form is used to report your tax identification number to the IRS. If you don’t file a W9 form by the October 2024 deadline, you may face penalties. The W9 Form October 2024 penalties for non-compliance can be substantial, so it’s important to file on time.

Catch-Up Contributions for 2024 and 2025

If you’re 50 or older, you can make additional contributions to your 401(k) plan beyond the regular contribution limit. These “catch-up” contributions are designed to help older workers save more for retirement, especially if they’ve fallen behind in their savings.

If you’re retired, you may have different tax rules than those who are still working. Use a tax calculator for retirees in October 2024 to estimate your tax liability and plan accordingly.

Catch-Up Contribution Limits for 2024 and 2025

The catch-up contribution limit allows individuals aged 50 and over to contribute an additional amount to their 401(k) plan on top of the regular contribution limit. This extra contribution can help them accumulate a larger retirement nest egg. Here’s a breakdown of the catch-up contribution limits for 2024 and 2025:

| Year | Regular Contribution Limit | Catch-Up Contribution Limit | Total Contribution Limit |

|---|---|---|---|

| 2024 | $22,500 | $7,500 | $30,000 |

| 2025 | $23,000 | $7,500 | $30,500 |

For example, if you’re 55 years old in 2024, you can contribute up to $30,000 to your 401(k) plan. This includes the regular contribution limit of $22,500 and the catch-up contribution limit of $7,500.

Students often have different tax situations than other taxpayers. Use a tax calculator for students in October 2024 to estimate your tax liability and plan accordingly.

Impact of Contribution Limits on Retirement Planning

Contribution limits play a crucial role in retirement planning, influencing the amount of money you can save and the potential growth of your retirement nest egg. Understanding these limits and strategically maximizing your contributions within them can significantly impact your financial well-being in retirement.

There may be tax changes that impact the October 2024 deadline. Stay informed about the tax changes impacting the October 2024 deadline to ensure you file your taxes on time and avoid penalties.

Maximizing Contributions Within Limits

It’s essential to take advantage of the full contribution limits to maximize your retirement savings. Here are some strategies to achieve this:* Increase Contributions Gradually:Start by contributing a small amount and gradually increase your contributions over time, as your income grows.

IRA contribution limits can change each year. The IRA limits for October 2024 have been adjusted for inflation, so you can potentially save more for retirement.

This can help make saving feel more manageable and less of a burden.

Rental income can be a great source of passive income, but it can also lead to a tax bill. Use a tax calculator for income from rental properties in October 2024 to estimate your tax liability and plan accordingly.

Automate Contributions

If you exceed the IRA contribution limits, you may face penalties. The penalties for exceeding IRA contribution limits can be significant, so it’s important to stay within the limits.

Set up automatic contributions from your paycheck to your 401(k) account. This ensures that you consistently save a portion of your income without having to manually make contributions.

Consider Catch-Up Contributions

High earners may have a higher limit on how much they can contribute to their 401(k) each year. The 401(k) contribution limits for 2024 for high earners are important to be aware of so you can maximize your retirement savings.

If you’re 50 or older, you can contribute additional amounts beyond the regular limit. This can help you make up for lost time and accelerate your savings.

The amount you can contribute to your 401(k) each year depends on your age and income. The amount you can contribute to your 401(k) in 2024 may have changed from previous years, so it’s important to check the limits.

Review Your Contribution Rate Regularly

If you’re a high earner, you may have a higher limit on how much you can contribute to your 401(k) each year. The 401(k) contribution limits for 2024 for high earners can help you save even more for retirement.

As your income increases, consider increasing your contribution rate to maximize your savings potential.

Impact of Contribution Limits on Retirement Savings Goals

Contribution limits can directly influence your retirement savings goals. Here’s how:* Reduced Savings Potential:If contribution limits are low, it can limit your ability to save enough for retirement. This can make it challenging to reach your desired retirement income level.

The tax brackets for 2024 have been adjusted to reflect inflation. The tax bracket changes for 2024 may affect your tax liability, so it’s important to stay informed.

Increased Time Horizon

If you’re self-employed, you can contribute to a Solo 401(k) to save for retirement. The IRA contribution limits for Solo 401(k)s in 2024 are higher than in previous years, so you can potentially save more for your future.

Lower contribution limits may necessitate a longer time horizon for your retirement savings to grow. This can require delaying retirement or adjusting your lifestyle expectations.

Importance of Early Saving

If you’re retired, you may have a different tax deadline than those who are still working. The October 2024 tax deadline for retirees is important to be aware of so you can file your taxes on time.

Contribution limits highlight the importance of starting to save early. The longer you save, the more time your money has to grow, potentially offsetting the impact of limited contribution amounts.

Factors Affecting Contribution Limits

While 401(k) contribution limits are set annually by the IRS, various factors can influence these limits. These factors play a crucial role in shaping retirement savings strategies for individuals and employers alike.

The standard deduction is the amount of income you can deduct from your taxable income. The standard deduction for 2024 has been adjusted for inflation, so it may be higher than in previous years.

Government Regulations

The IRS sets the annual contribution limits for 401(k) plans. These limits are adjusted annually to reflect inflation and other economic factors. The government’s role in setting these limits is crucial to ensure fairness and promote retirement savings across the workforce.

Government regulations aim to ensure that individuals have sufficient opportunities to save for retirement while balancing the need to maintain fiscal responsibility.

Employer Contributions, What are the 401k contribution limits for 2024 and 2025

Employer contributions to 401(k) plans can significantly impact individual contribution limits. In some cases, employers may offer matching contributions, where they contribute a certain percentage of an employee’s salary to their 401(k) account. These matching contributions are typically subject to limits, which can influence the total amount an individual can contribute to their 401(k) plan.

For example, if an employer offers a 100% match up to 5% of an employee’s salary, an employee who contributes 5% of their salary will receive an additional 5% from their employer. This means the employee’s total contribution limit may be higher than the standard limit due to the employer’s matching contribution.

Concluding Remarks: What Are The 401k Contribution Limits For 2024 And 2025

In conclusion, understanding the 401(k) contribution limits for 2024 and 2025 is essential for anyone looking to maximize their retirement savings. By staying informed about the latest regulations and taking advantage of available options, individuals can make informed decisions about their financial future.

Remember to consult with a financial advisor for personalized guidance on your specific circumstances.

General Inquiries

What is the difference between a traditional 401(k) and a Roth 401(k)?

A traditional 401(k) allows you to contribute pre-tax dollars, which lowers your taxable income in the present. You’ll pay taxes on the money when you withdraw it in retirement. A Roth 401(k) allows you to contribute after-tax dollars, meaning you won’t owe taxes on the money when you withdraw it in retirement.

Can I contribute to both a traditional and Roth 401(k) at the same time?

No, you can only contribute to one type of 401(k) at a time. However, you can switch between traditional and Roth 401(k) plans, subject to certain rules and restrictions.

What happens if I exceed the 401(k) contribution limit?

If you exceed the contribution limit, you may be subject to penalties and taxes. The excess contributions will be considered taxable income in the year they were made. You may also have to pay a 10% penalty on the excess contributions.